This year, the number of A-share delisting companies has reached a record, and the stock market has accelerated its efforts to absorb new ideas.

This year, the capital market is accelerating the process of expelling the old and absorbing the new. On the one hand, delisting stocks are increasing, and at least 12 companies may be delisted or in the delisting period this year. "Fraudulent retreat", "broken retreat" (the stock price falls below the face value), "performance retreat", "active retreat" and "reorganization retreat" are endless; On the other hand, the IPO in the A-share market is moving towards normalization. This year, 120 companies have completed the issuance of the main board, small and medium-sized board and Growth Enterprise Market, and 56 companies have officially listed and traded in science and technology innovation board.

The number of delisting companies has increased greatly.

This year, there has been a new situation in the delisting of A-shares, not only in terms of quantity, but also in terms of types. Fraud retreat, face-breaking retreat, performance retreat, initiative retreat and reorganization retreat all appear.

In May of this year, the Shanghai Stock Exchange decided to terminate the listing of the shares of *ST Hairun and *ST Shangpu in accordance with the law; On the same day, the Shenzhen Stock Exchange decided to terminate the listing of the shares of *ST Hua Ze and *ST Zhonghe in accordance with laws and regulations. At present, these four stocks have been delisted by the market. On November 8, the official website of Shenzhen Stock Exchange published the Announcement of Changsheng Biotechnology Co., Ltd. on the Bankruptcy and Liquidation of the Company’s wholly-owned subsidiaries, declaring Changchun Changsheng Biotechnology Co., Ltd. bankrupt. On the evening of November 26th, Changsheng Bio (i.e. Growth Retirement and *ST Changsheng) issued the Announcement on the Delisting and Delisting of the Company’s Stock, saying that the company’s stock had been decided by Shenzhen Stock Exchange to terminate its listing and delisted by Shenzhen Stock Exchange on November 27th, 2019.

On December 2, Hunan Qian Shan Pharmaceutical Machinery Co., Ltd. disclosed the Announcement on Receiving from China Securities Regulatory Commission, and made a special risk warning: according to the facts identified in the notice in advance, the company’s net profit for four consecutive years from 2015 to 2018 was actually negative, which touched on the situation of mandatory delisting of listed companies in Shenzhen Stock Exchange under Article 4 (3) of the Implementation Measures for Mandatory Delisting of Listed Companies in Major Violations, and the company’s shares may be subject to mandatory delisting in major violations.

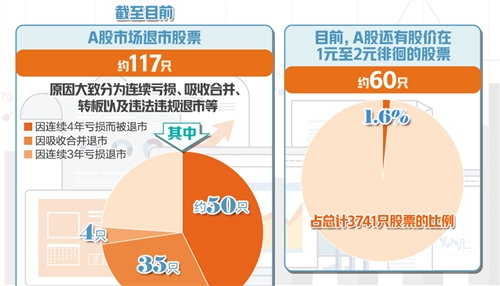

Up to now, there are about 117 delisted stocks in the A-share market, and the reasons are roughly divided into continuous losses, mergers and acquisitions, transfer of shares and illegal delisting. Among them, about 50 companies were delisted due to losses for four consecutive years, followed by about 35 stocks delisted due to merger. In addition, four companies were delisted due to losses for three consecutive years.

Chen Li, director of Chuancai Securities Research Institute, said that this year, in addition to the regular situation that the performance has been losing money or even insolvent for many years, there are also companies that have been delisted due to fraudulent issuance and illegal information disclosure, and companies that have been terminated due to the "inability to express opinions" issued by accounting firms, and there have been two major illegal delisted companies, namely Changsheng Bio and Qian Shan Yaoji.

"Face value delisting" has gradually become the norm.

It is worth noting that this year’s A-share market has been delisted at face value (the closing price of stocks for 20 consecutive trading days is lower than face value, triggering delisting).

On December 4th, Shanghai Stock Exchange made a decision to terminate the listing of shares of Beijing Huaye Capital Holding Co., Ltd. (hereinafter referred to as *ST Huaye or the company) in strict accordance with the relevant provisions of the Listing Rules.

* The termination of listing of ST Huaye’s shares due to the reason that the share price continues to be lower than the face value is a true reflection of the company’s fundamentals and a choice of the market. Huaye Company is mainly engaged in real estate development business, medical investment business and mining investment business. Last year, it encountered contract fraud, involving 10.189 billion yuan, which directly caused the accounts receivable to be partially or completely unrecoverable. Last year, the company suffered a huge loss of 6.4 billion yuan, and in the first three quarters of this year, it lost another 5 billion yuan. The stock price fell all the way to trigger "face value delisting".

On the evening of August 19th, Shenzhen Stock Exchange announced the termination of listing of *ST Young Eagle, which became the second "delisting" stock in the A-share market. On September 11th, *ST Seal also touched the "face value delisting" rule, and its company’s stock was decided by Shenzhen Stock Exchange to terminate its listing on October 10th, and entered the delisting consolidation period on October 18th. *ST Dakong also announced on October 25 that the Shanghai Stock Exchange has decided to terminate the listing of the company’s shares.

At present, there are about 60 A-share stocks, such as *ST Pegasus, ST Ruidian, *ST Huge and *ST Opal, hovering from 1 yuan to 2 yuan, accounting for about 1.6% of the total of 3,741 stocks, which are always threatened by "face value delisting".

According to Zhang Qiang, CEO of Huiyan Huiyu Asset Management Company, stocks with "face value delisting" have three characteristics: the fundamentals of such companies have deteriorated, and they often have the title of ST shares or *ST shares; In the case of continuous deterioration of operations, many companies are still keen on capital operations such as cross-border acquisitions; Companies with "face value delisting" basically have risk factors, such as violation of laws and regulations, blind expansion, business deterioration, debt default, capital occupation, issuance of non-standard audit opinions on annual reports, investigation by the Securities and Futures Commission, and notification by the Shanghai and Shenzhen Stock Exchanges, but they have not been highly valued by the company’s management.

“‘ Delisting at par value ’ It has gradually become the norm in the A-share market, and junk stocks have changed from ‘ Delisting is difficult ’ Become ‘ Difficult to keep the shell ’ , highlighting the continuous marketization, normalization and rule of law of the delisting system, investors ‘ Vote with your feet ’ It has become one of the main ways to improve the self-purification ability of the market. " According to Li Rui, a professor at the School of Economics and Business Administration of Beijing Normal University, the number of "face value delisting" stocks continues to increase, which deserves the deep vigilance of listed companies. Listed companies should do their main business in a down-to-earth manner, attach importance to endogenous innovation and growth, stay away from blind cross-border mergers and acquisitions, "speculation concepts", and strictly adhere to the bottom line of market risk.

Conducive to market self-purification

Capital market, like enterprises, has a life cycle, and the basic law of "metabolism" is also applicable, so that the healthy and stable development of the entire capital market ecosystem can be realized by "life and death".

Since the beginning of this year, A-share IPO issuance has always maintained a steady pace. By December 4th, this year, a total of 120 companies in the main board, small and medium-sized board and Growth Enterprise Market had completed the issuance, with an average of 2.7 companies issued every week, raising 3.69 billion yuan, a slight increase over the same period last year. The number of enterprises in science and technology innovation board has reached 100. Among them, there are 56 listed companies in science and technology innovation board, and 8 quasi-listed companies are in the stage of subscription and roadshow. Other companies are waiting for the registration approval of the CSRC.

Zhang Qiang believes that with the development and improvement of China’s financial system, the reform of the A-share delisting system is also deepening. The number of companies delisted this year has increased significantly compared with previous years, which is in stark contrast to the phenomenon of "protecting the shell and buying the shell" and "returning to life" in previous years. At present, the regulatory authorities strictly delist enterprises with financial irregularities and long-term performance losses through multiple dimensions, coupled with the continuous issuance of new shares, which has changed the original situation that listing is difficult and delisting is more difficult, and improved the self-purification ability of A-shares, which is a sign that the stock market is maturing.

"From the perspective of development, the reasonable arrangement of delisting of listed companies by the system can free up market space for high-quality enterprises, which is the embodiment of the maturity of the national capital market. Since the beginning of this year, there have been many measures to reform the basic system of China’s capital market, and the results have been good. The marketization, normalization and legalization of the delisting system will be the general trend. " Chen Hao said.

The spokesman of Shenzhen Stock Exchange also said that the delisting system of listed companies is an important operating mechanism for the capital market to achieve survival of the fittest and optimize the allocation of resources, and it is also a basic arrangement for clearing market risks and purifying the market environment, which is conducive to improving the quality of listed companies.